Are You Guilty of These 5 Common Finance Mistakes? Find Out How to Fix Them

Common Finance Mistakes 1 – Client Onboarding.

At the very start before doing any work make sure you find out your client’s full name, postal address, email address and contact number. Also find out specifics on invoices the client may have such as reference numbers, who to send the invoice to for payment etc.

Just a first name and an email address give you few other options to chase up your money and some clients do not pay unless you follow their invoicing procedures to the letter, so it is best to find out what they are before you start.

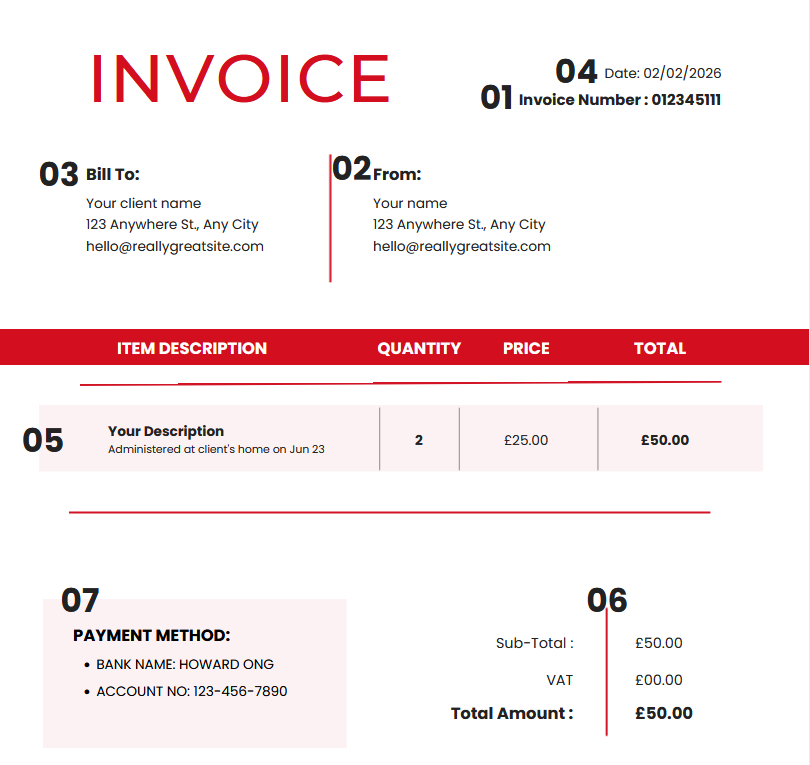

Common Finance Mistakes 2 – Sending Out Invoices.

You’ve done the work, don’t forget to send out the invoice!

It is quite amazing how many business owners miss this step. I had a client who was having cashflow issues and got me in to help him, it turned out they had not sent out any invoices for the last 7 months.

Send out your invoices as soon as you have done the work or have a set invoicing day each month to make sure you get them out whilst they are still in your mind.

Common Finance Mistakes 3 – Make It Easy For Clients To Pay You.

Make it easy for clients to pay you by including invoice numbers, due dates, total amounts and how to pay you. Also put in a breakdown/explanation of the costs so it is clear what you are invoicing for.

Linking your accounts package with Paypal or similar does add a little extra expense with the transaction fees but is loved by clients as all they have to do is click on the big green button, confirm their details and boom the payment is made.

Common Finance Mistakes 4 – Access To Banking.

Don’t just have one person with login details to the bank account and or one person as signatory for payments.

At best if the person is ill, you will have a delay to finding how much is in your account and also will not be able to pay your suppliers until they return.

At worst if the person leaves you will have no access to your financial information as the bank will only talk to the registered contact and you will have to go through a long and stressful process of proving who you are to get access to run the account.

So always have multiple signatories with full access logins to your bank accounts then if one person is ill or leaves payments can still be made and the usual bank reconciliation tasks can be kept up to date.

Common Finance Mistakes 5 – Not Double Checking Things.

Not just once a year with sending stuff to your accountant for the statutory reports to be completed but regularly check the work in your finance department. At worst by not keeping an eye on things when you do look you can find out your teasurer/accountant has been making unauthorised payments to themselves or 3rd parties. But even when there is no malice or fraudulent activities taking place a whole host of things can happen such as:-- Owners spending more than they thought they had due to not seeing any financial reports.

- Payments get missed.

- Payments get sent to the wrong place as the details were not checked before sending off.

I had a sad story to deal with from a client who asked me to do some profit and loss accounts for their business. The husband had been doing all the accounts stuff on his own and the wife became alerted to things not being paid etc and it turned out the husband had been suffering from the onset of dementia for a couple of years. Lucky it has now be caught and he is getting the support needed and the bills are getting paid.